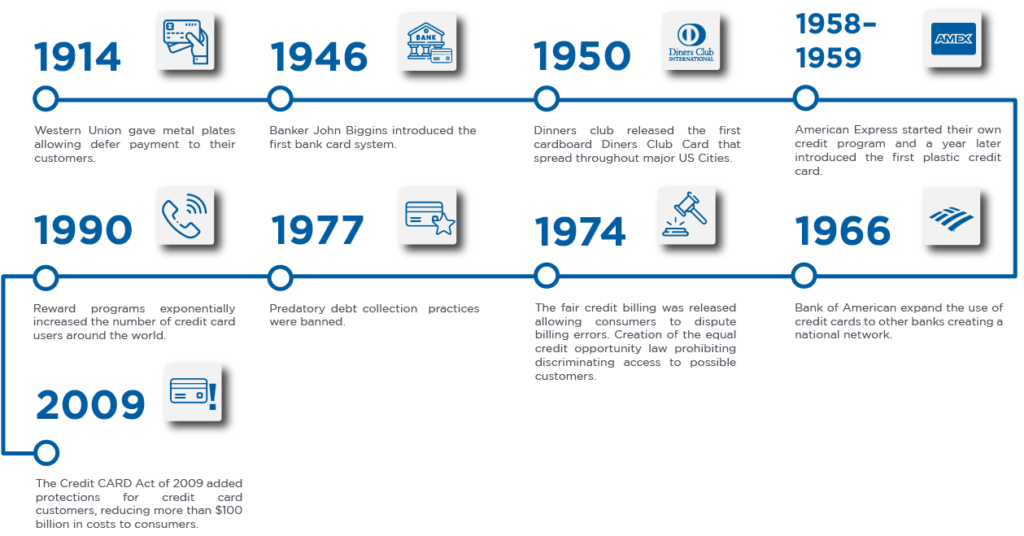

The concept of credit was born from the idea that a monthly payment plan would allow consumers to obtain goods that were otherwise unaffordable. Companies like Singer and Ford were the first to introduce buying on credit to U.S. consumers.

$183.32 billion

$49.69 billion

$166.32 billion

$36.36 billion

$106.74 billion

$29.36 billion*

$88.02 billion

$60.08 billion

$60.08 billion

$49.69 billion

As stated, credit reports contain the most significant information related to your credit behavior and legal issues in reference to your finances. Credit granters can also access:

- Credit history.

- Public records.

- Inquiries Personal Information.

- Current and previous addresses.

- Current and previous employers.

- List of the credit accounts from the last ten years.

- Tax liens.

- Bankruptcies.

- Court judgments(including child support judgments).

- List of creditors or authorized users who have requested a copy of your credit report.

- List of inquiries made by the user when seeking loan or credit.

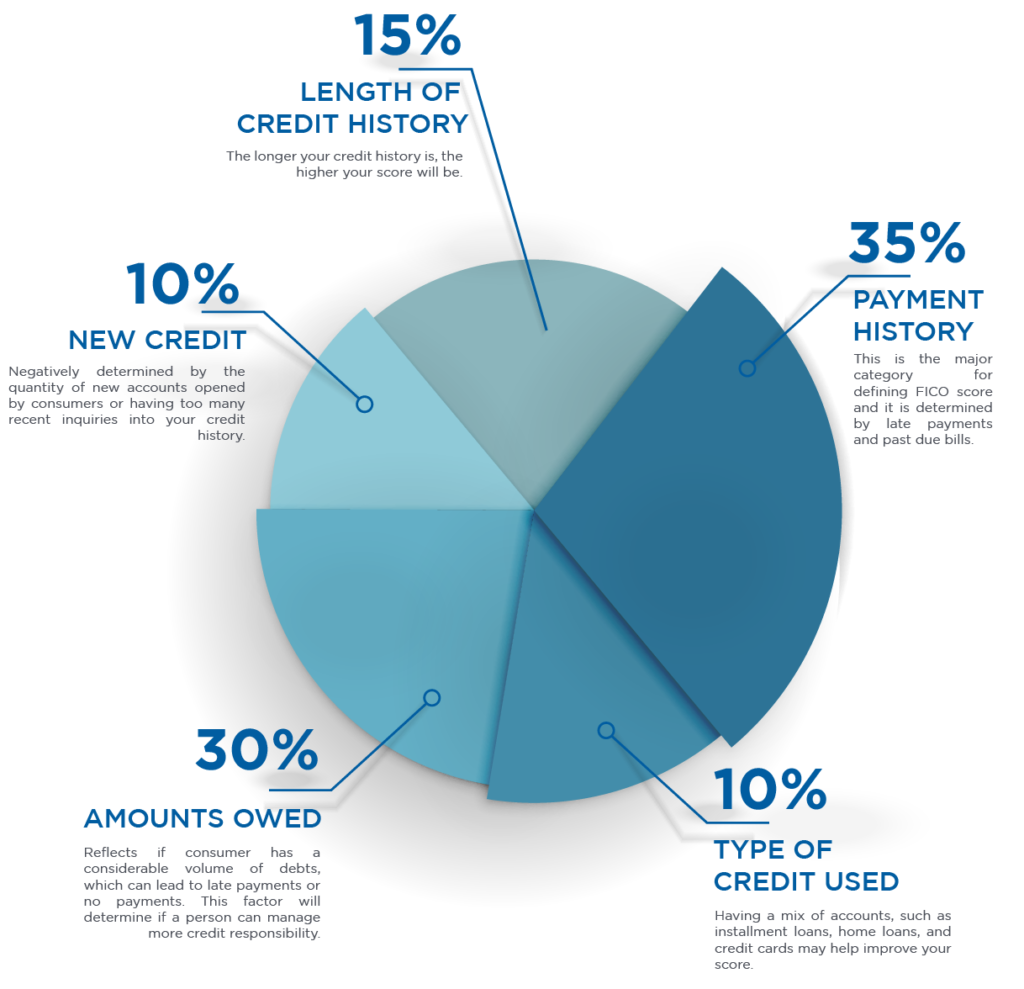

The most used scoring system is FICO which stands for The Fair Isaac Company. The FICO system has five major categories that make up a credit score.

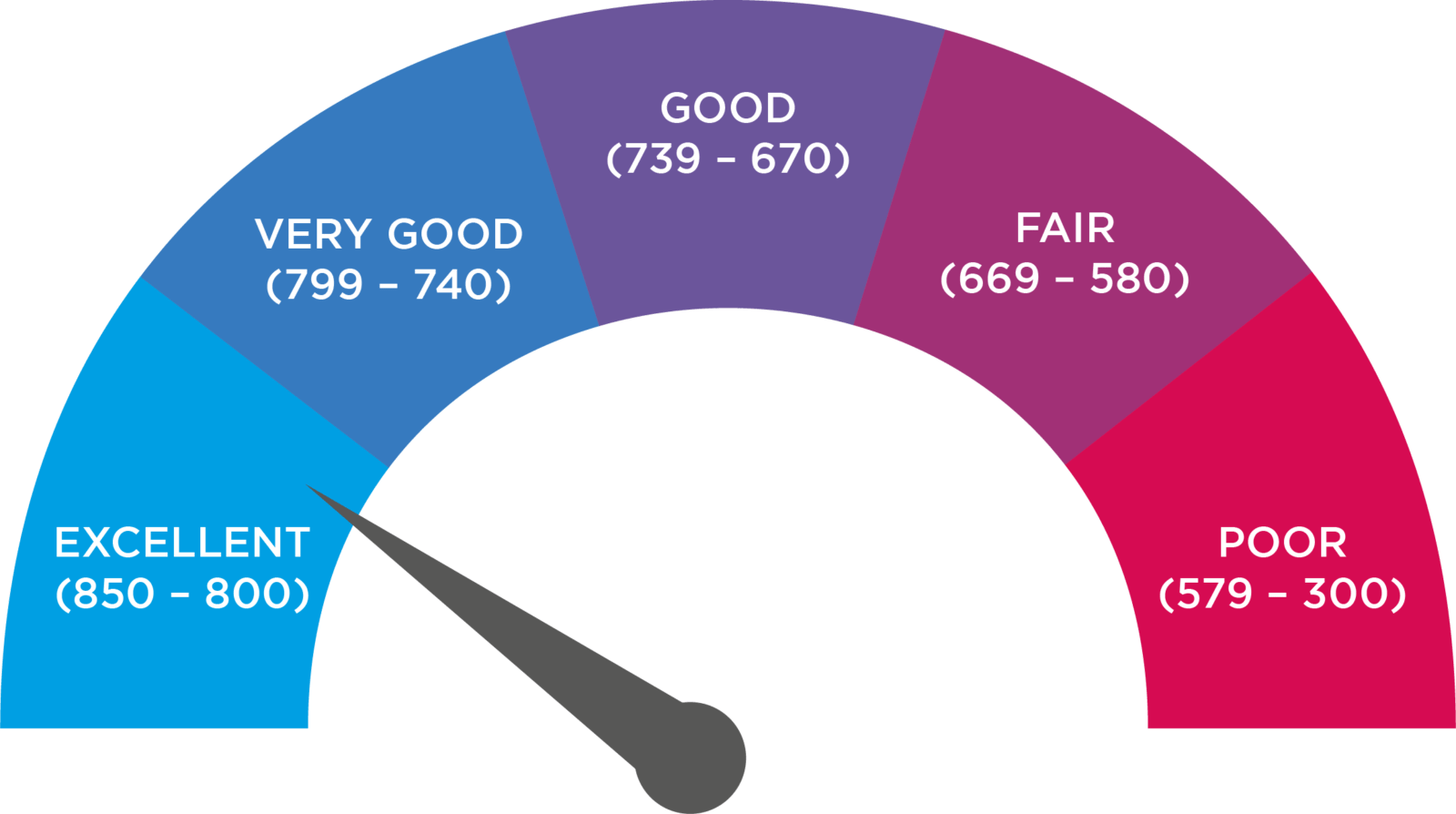

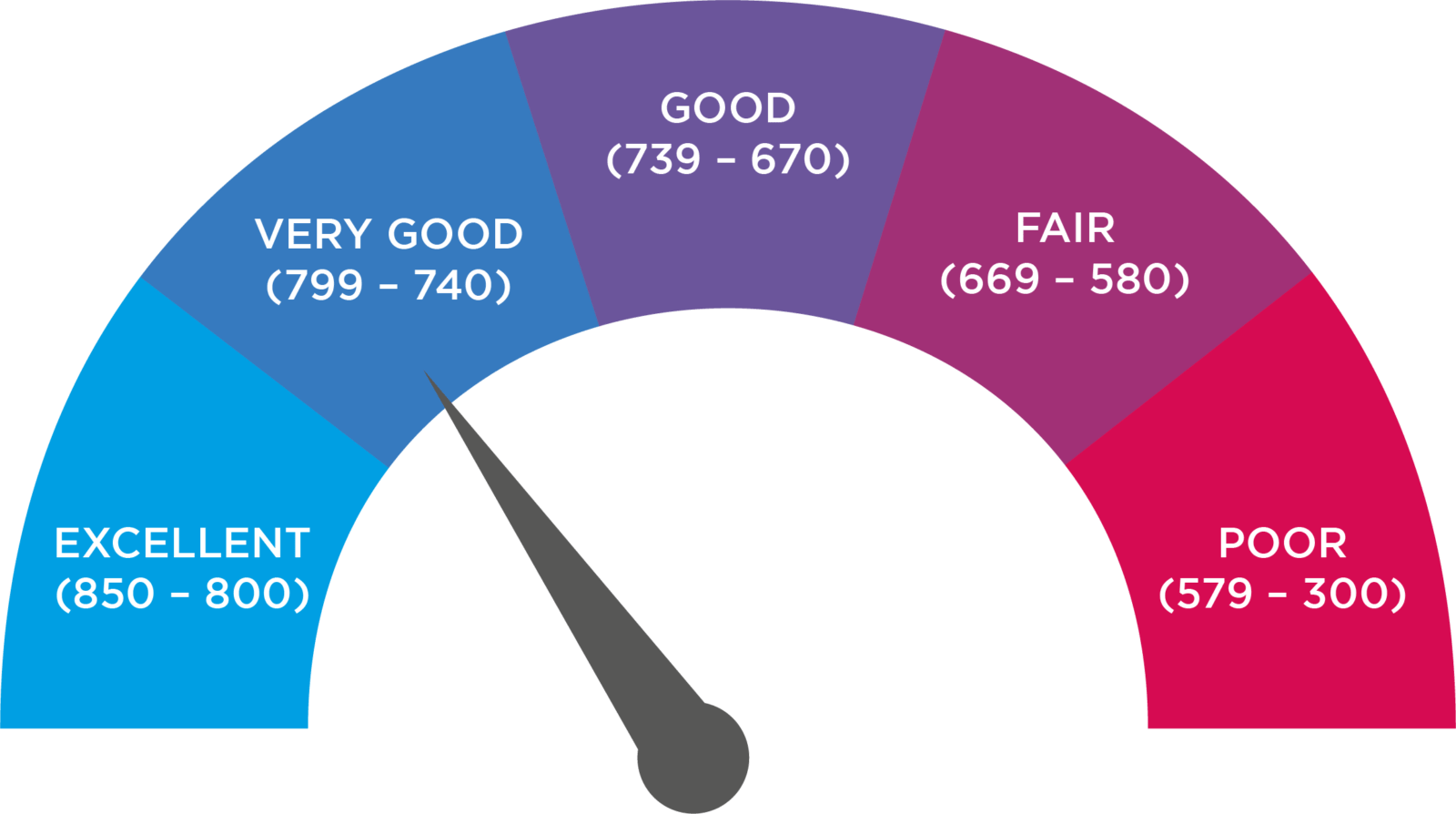

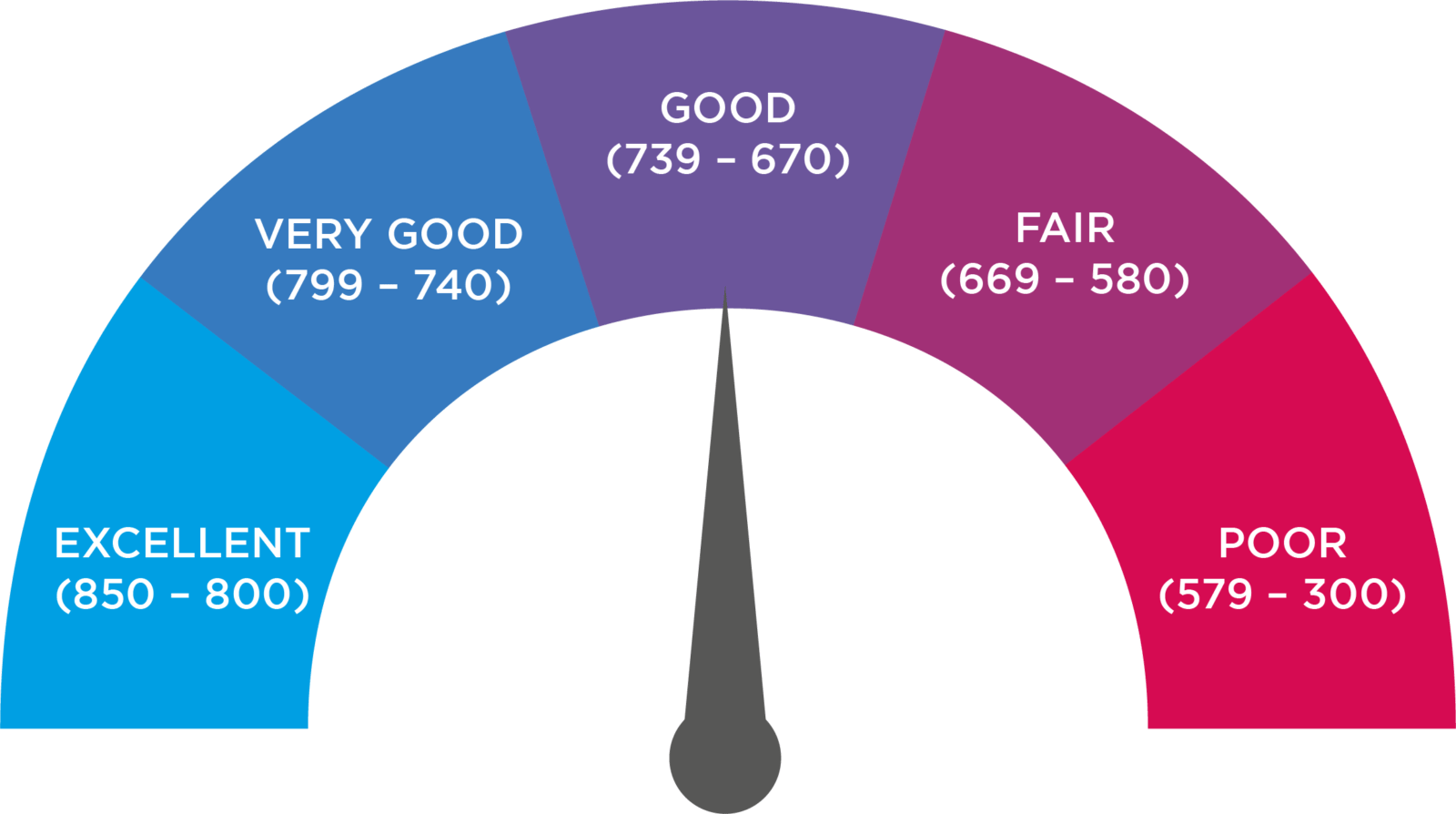

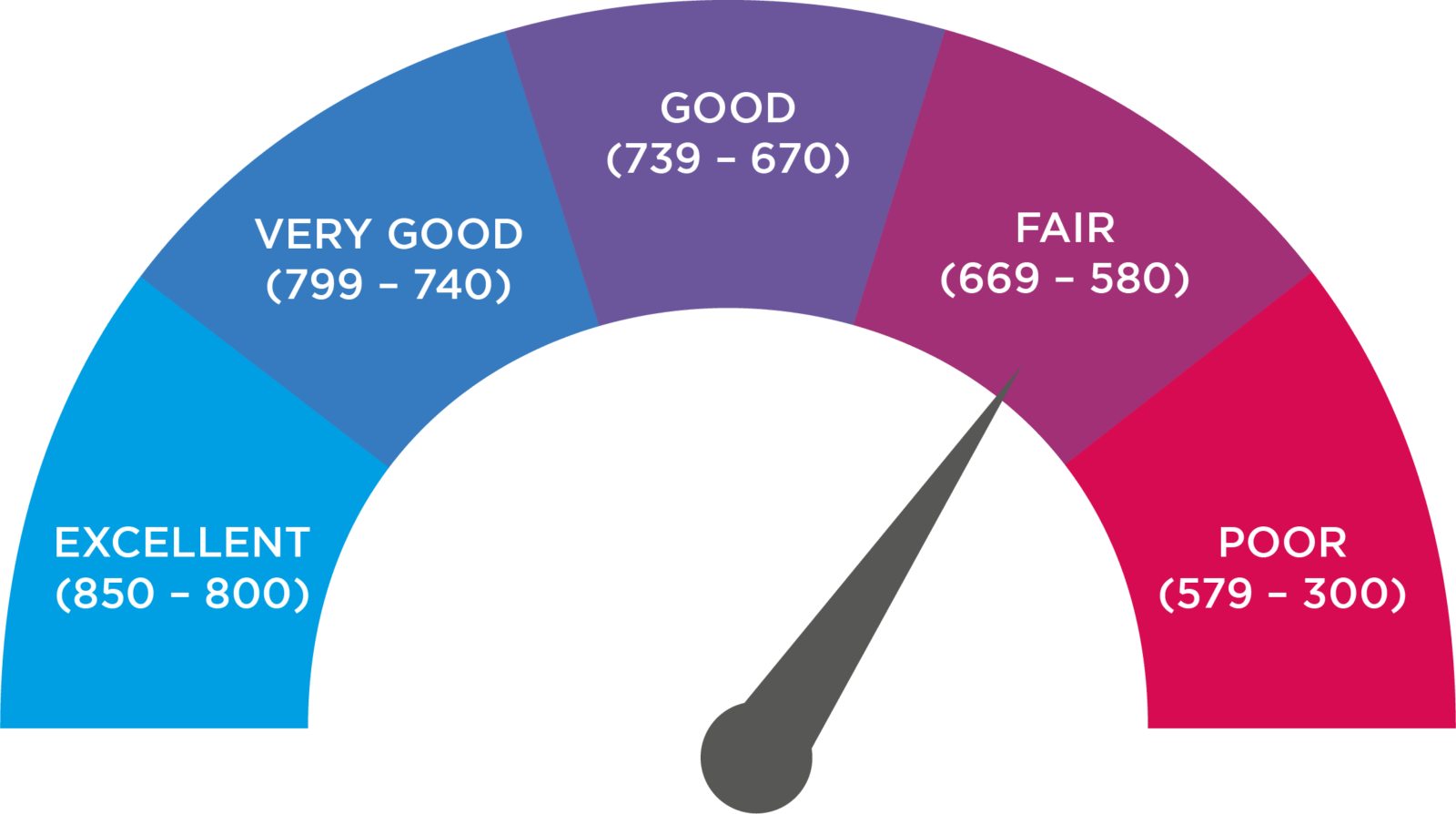

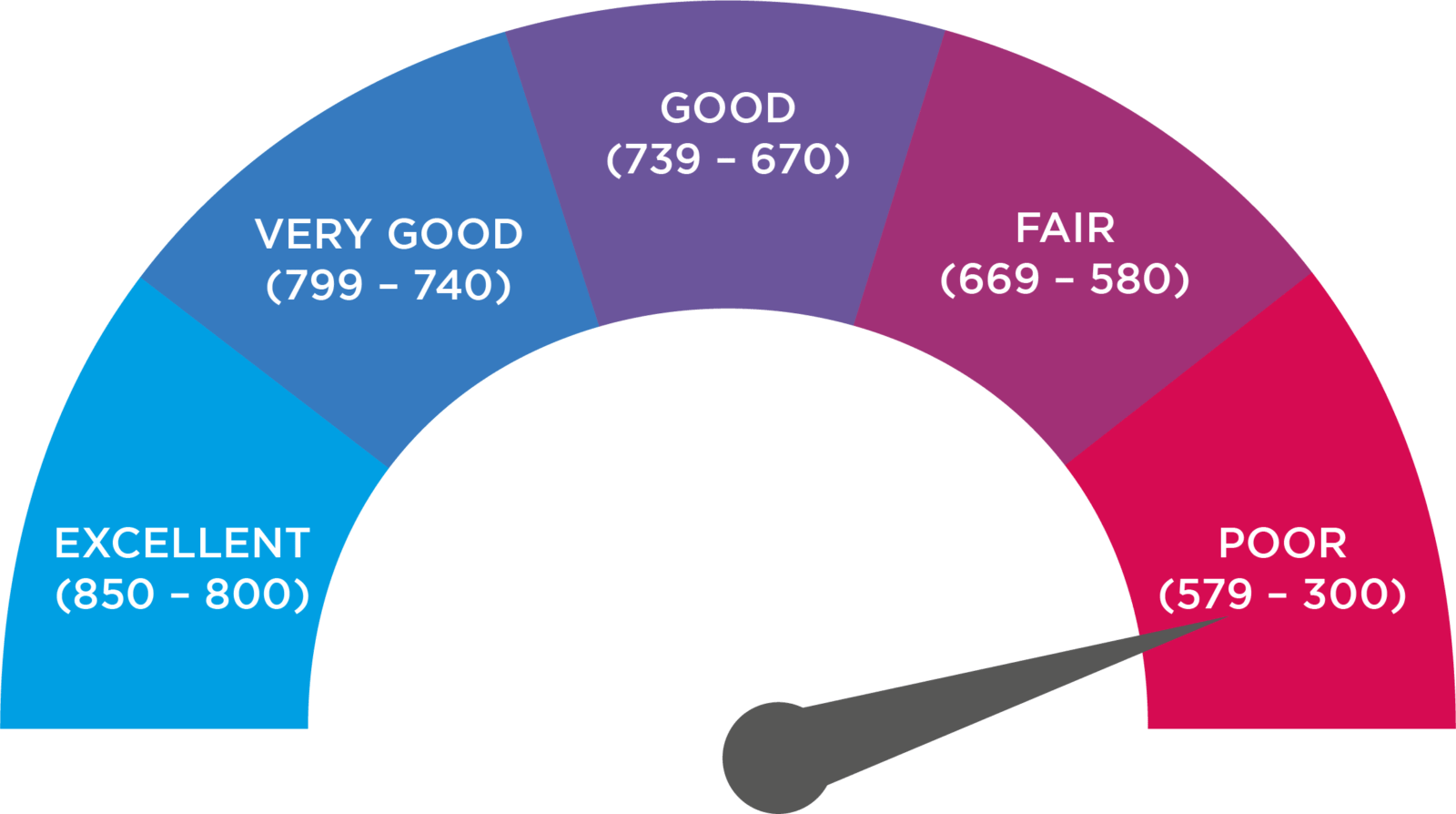

Credit rating is the numerical translation of your credit report. A number between 850 to 300 is used as a score to rates all your credit information, the higher number, the better.

This “number” known as a FICO score can easily impact or prevent you from getting a job, an apartment, or even increase the cost of your insurance. So, keeping a good score is something you must pay attention to.

(850 – 800)

This is an excellent credit score range and will give you an open window to credit with good interest rates.

The first step into is contacting us. Remember that our service has no cost and no restriction regarding the amount of debt, annual income or credit score.

After speaking with one of our certified counselors, you will be asked general questions regarding your financial situation. There will be a step-by-step review of your debts, income and expenses, and you will receive a budget that fits your specific situation.